Does Insurance Cover IVF: What you Need to Know

Quick answer: Sometimes. IVF insurance coverage depends on where you live, your employer, and whether your health plan is fully insured or self-funded. Some states require IVF coverage, but many plans are exempt, meaning a large number of patients still pay out of pocket.

The cost of in vitro fertilization (IVF) can be a major concern for individuals and couples pursuing fertility treatment. Whether insurance will help cover those costs depends on several factors, including state laws, employer benefits, and the structure of your insurance plan.

In this article, we’ll explain how IVF insurance coverage works, which states mandate coverage, why many people remain excluded even in mandate states, and what options exist if insurance does not cover IVF.

What Does Insurance Cover?

Approximately 25% of Americans have insurance that includes coverage for IVF treatments specifically.

However, many more have plans that cover certain aspects of the IVF process, such as diagnostic testing, monitoring, or other related services, which can help reduce overall out-of-pocket costs.

While some insurance policies exclude all fertility-related expenses, others may provide coverage for related treatments, part of IVF, or the full spectrum of care, including:

- Diagnostic testing to identify fertility issues

- Diagnostic testing and some less costly/invasive treatments like IUI (aka artificial insemination).

- Medications used for ovarian stimulation.

- Monitoring appointments during the IVF cycle.

- Full or partial coverage for the entire IVF process, including diagnostic testing, medications, egg retrieval, laboratory fertilization, and embryo transfer.

Three Factors That Determine IVF Insurance Coverage

If you’re trying to answer the question “Does insurance cover IVF?” It almost always comes down to three factors.

- Employer-provided benefits

Some employers choose to include fertility benefits regardless of state law. Larger employers and companies in certain industries are more likely to offer IVF coverage as part of their health plans. - State IVF mandates

Some states require insurers to cover IVF, but these laws vary widely and often include strict eligibility requirements or exclusions. Even inmandate states, coverage is far from universal. - Your insurance plan type

This is the factor that surprises most patients. There are three common plan structures:

- Private or fully insured employer plans

These plans are regulated by state law and must follow state IVF mandates when applicable.

- Private or fully insured employer plans

- Self-funded employer plans

In these plans, the employer pays healthcare claims directly and assumes the financial risk. These plans are governed by federal law and are exempt from state IVF mandates, even if the employer is located in a mandate state. This exemption is one of the most common reasons patients discover they do not have IVF coverage despite living in a state with mandated benefits.

- Self-funded employer plans

How to Confirm Your Coverage

To determine whether IVF is covered under your plan, review your benefits carefully and contact your insurance provider or HR department. Be sure to ask about:

- Coverage for IVF and related fertility treatments

- Coverage for fertility medications

- Deductibles, copays, and lifetime or cycle limits

- Prior authorization or diagnostic requirements

Keep in mind that even when IVF is technically covered, high deductibles can mean spending $10,000 or more out of pocket before benefits apply.

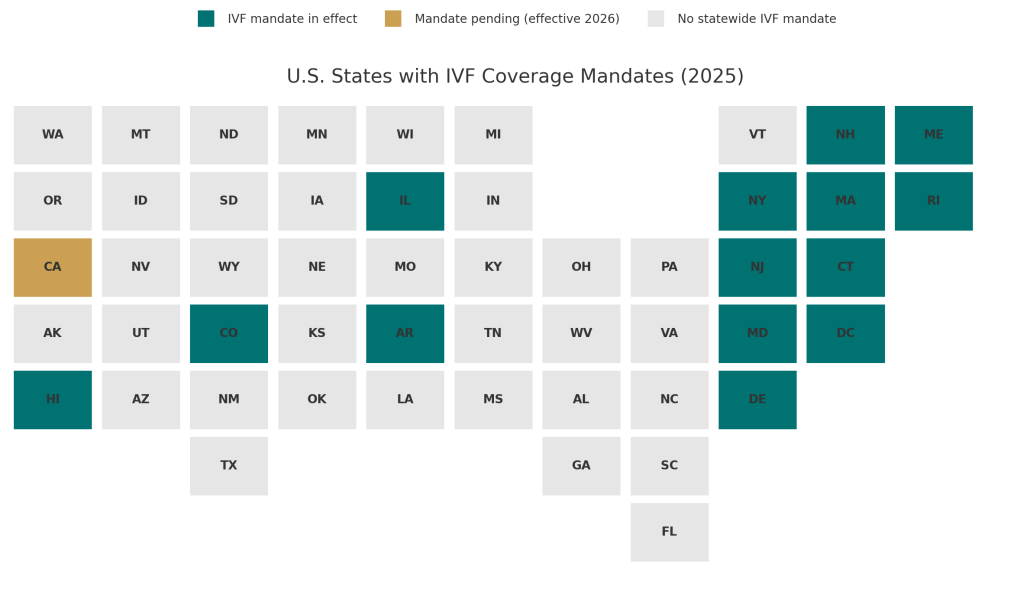

IVF Insurance Coverage by State

A growing number of states have laws mandating some form of fertility coverage. However, the services that are included or excluded from these mandates vary widely from state to state.

According to the National Fertility Association, as of April 2025, 22 states plus Washington, D.C. have passed fertility insurance coverage laws, and 15 of those laws include IVF coverage to some degree.

Many of the laws mandating IVF coverage are written in a way that excludes a large percentage of people from coverage.

For example, most laws exclude plans offered by employers with fewer than 100 employees; according to the United States Small Business Administration, this alone leaves out approximately half the workforce.

Here’s a brief overview of the laws in states where IVF coverage is mandated in some form.

| State | IVF Coverage Mandated | Key Limits and Exemptions |

|---|---|---|

| Arkansas | Yes | $15,000 lifetime cap. Requires 2 years of infertility or qualifying diagnosis. Must use spouse’s sperm. Less costly treatments required first. |

| California | Yes (effective July 2025) | Applies to large group plans only. Covers up to 3 egg retrievals and unlimited transfers. Small employers exempt. |

| Colorado | Yes | Applies to large group plans. Covers up to 3 retrievals and unlimited transfers. Must follow ASRM guidelines. Self-funded employers exempt. |

| Connecticut | Yes | Covers IVF and IUI. Limited to patients under 40. Two IVF cycles lifetime maximum. |

| Delaware | Yes | Covers up to 6 retrievals with unlimited transfers. Covers donor egg cycles. Small and self-funded employers exempt. |

| Hawaii | Yes | Covers one IVF cycle with strict infertility criteria. Requires spouse’s sperm and failure of other treatments. Self-funded plans exempt. |

| Illinois | Yes | Covers 4 retrievals, plus 2 more after a live birth. Employers under 25 employees exempt. Self-funded plans exempt. |

| Maine | Yes | Covers infertility diagnosis, IVF, and fertility preservation for medical necessity. |

| Massachusetts | Yes | Covers up to 6 retrievals per lifetime. Self-funded employers and some religious organizations exempt. |

| Maryland | Yes | Up to 3 IVF attempts per live birth. $100,000 lifetime cap. Requires infertility diagnosis and prior treatments. |

| New Hampshire | Partial | Covers medically necessary fertility care. IVF may require prior treatment attempts. Individual and small plans exempt. |

| New Jersey | Yes | Covers 4 retrievals per lifetime. Patient must be 45 or younger. Small employers exempt. |

| New York | Yes | Large employers must cover up to 3 IVF cycles. Frozen transfers count toward the cycle limit. |

| Rhode Island | Yes | Coverage ages 25–42. $100,000 lifetime cap. Includes fertility preservation. |

| States without mandates | No | Coverage depends entirely on employer benefits or private insurance design. |

Below is a closer look at how these mandates actually work in practice, including common exclusions and eligibility requirements that affect real patients.

Arkansas

Arkansas has a $15,000 lifetime max for fertility coverage. This covers IVF, but has the following stipulations:

- The individual or couple must have at least a 2-year history of infertility, or the infertility must be caused by a diagnosis of endometriosis, blocked or surgically removed fallopian tubes (not from an elective tubal ligation), DES exposure, or abnormal male factors.

- The woman’s eggs must be fertilized by the sperm of their spouse.

- The patient must have tried and failed to get pregnant through less expensive treatments. This means that the majority of that $15,000 will likely be used before IVF on less costly, but far less effective treatments, like IUI.

California

The new California law, SB 729, requires coverage for infertility diagnosis and treatment, including IVF (up to three completed egg retrievals and unlimited embryo transfers) for fully insured large-group plans.

However, implementation has been delayed. Rather than going into effect July 1, 2025, the mandate now takes effect for policies issued, amended, or renewed on or after January 1, 2026.

Some policies that renew between July 1, 2025, and December 31, 2025, may voluntarily include fertility services even before the mandate goes into effect.

California law also broadens the definition of infertility to include single women, single men, and same-sex couples.

Meanwhile, California has applied to expand its essential health benefits (EHBs) to include fertility services in the individual and small group markets starting in 2027 (pending federal approval). This would be a huge win for millions of people in markets that are nearly universally excluded in other state and national mandates.

Colorado

Colorado mandates that all large group health benefit plans issued or renewed on or after January 1, 2023, provide coverage for infertility diagnosis, treatment, and standard fertility preservation services, including up to three completed oocyte retrievals and unlimited embryo transfers. The law defines large group plans as 100 or more employees.

These plans must follow American Society for Reproductive Medicine (ASRM) guidelines and cannot impose higher costs, exclusions, or restrictions on fertility treatments compared to other medical services covered under the plan.

There are some exemptions to be aware of, including individual and small group policies, religious organizations, and employers who self-insure.

Connecticut

The Connecticut law is one of the most inclusive and comprehensive. It mandates coverage of both Individual and group health insurance policies and includes coverage for services such as IUI and IVF.

Some restrictions include:

- Under the age of 40

- Lifetime maximum of two IVF cycles

Delaware

Delaware’s insurance law includes up to 6 IVF retrievals with an unlimited number of transfers from those retrievals and also covers donor egg cycles.

Some restrictions include:

- Retrievals must be completed before the age of 45, and transfers before the age of 50.

- Employers who self-insure or have fewer than 50 employees are exempt from state requirements.

Hawaii

Hawaii has laws that mandate coverage of one cycle of IVF. However, this mandate is subject to many rules and stipulations.

- Coverage is only required if the patient or spouse has at least a 5-year history of infertility.

- If infertility is associated with one of the following conditions: endometriosis, DES exposure, blocked or surgically removed fallopian tubes, or abnormal male factors contributing to infertility.

- The eggs must be fertilized with the spouse’s sperm.

- Coverage is only given if other treatments failed.

- Self-insured employers are exempt from providing coverage.

Illinois

Each person is covered for four egg retrievals. However, if a live birth occurs in one of those cycles, two additional egg retrievals will be covered with a total lifetime maximum of six retrievals.

Exclusions include:

- Employers with fewer than 25 employees

- religious organizations

- Self-insured employers

Maine

Maine’s fertility insurance mandate requires coverage for:

- fertility diagnostic care

- treatments including IVF

- medically necessary fertility preservation services, such as egg or sperm freezing before procedures like chemotherapy.

Massachusetts

Each person is covered for four egg retrievals. However, if a live birth occurs in one of those cycles, two additional egg retrievals will be covered with a total lifetime maximum of six retrievals.

Some key details include:

- Infertility is defined as the inability to conceive after one year of unprotected intercourse for women aged 35 or younger, or after six months for women over 35.

- Self-insured employers and specific religious organizations are exempt from this mandate.

Maryland

Maryland requires individual and group insurance policies that provide pregnancy-related benefits to cover the cost of IVF with the following limitations.

- Coverage may be limited to three IVF attempts per live birth and have a lifetime maximum of $100,000.

- Must attempt to get pregnant with less expensive treatment options first.

- Must have at least a two-year history of infertility or have infertility caused by: endometriosis, blocked or surgically removed fallopian tubes (non-voluntary), abnormal male factors, or fetal exposure to diethylstilbestrol (DES).

- The male spouse’s sperm must be used to fertilize the woman’s eggs unless he is unable to produce or deliver functional sperm. This inability can’t be related to a voluntary vasectomy.

- For same-sex couples, there must be six previously failed attempts of artificial insemination over the course of two years, or have infertility related to one of the conditions mentioned above.

- Religious organizations may be exempt.

New Hampshire

Provides coverage for medically necessary fertility treatments. Coverage does not apply to individual health plans, plans available through the Small Business Health Options Program (SHOP), or Extended Transition to Affordable Care Act-Compliant Policies.

The law prohibits insurers from imposing coverage limitations based solely on arbitrary factors such as the number of attempts, dollar amounts, or age. However, insurers may require that patients undergo less costly, “medically appropriate” treatments before before IVF.

New Jersey

Coverage includes 4 Egg retrievals per lifetime and requires the patient to be 45 years of age or younger. Employers with less than 50 employees are exempt.

New York

Private health plans from employers with 100 or more full-time employees must provide coverage for up to three cycles of IVF (frozen embryo transfers count as a cycle).

As of 2025, a new bill, A.885, called the Equity in Fertility Treatment Act, aims to expand the definition of infertility and increase the number of people who can receive coverage for IVF treatment. But this bill is still in the early stages before passage into law.

Rhode Island

Coverage is provided for individuals between 25 and 42 years of age, with a $100,000 cap on treatment costs. The insurer may also charge a 20% co-payment.

Rhode Island was the first state to require coverage for fertility preservation services before medical procedures that impair fertility, such as chemotherapy or radiation. Preservation includes egg or sperm freezing.

Washington D.C.

Effective January 1, 2025, Washington, D.C. ratified a law called “Expanding Access to Fertility Treatment Amendment Act of 2023 (D.C. Law 25-49)“.

This requires all individual, small group, and large group health plans to cover the diagnosis and treatment of infertility, including in vitro fertilization (IVF) and standard fertility preservation services.

- At least three completed egg retrievals

- Unlimited number of embryo transfers resulting from those retrievals.

- IVF coverage also extends to embryo transfers into a third party (such as a gestational carrier), though it does not include unrelated medical costs of the surrogate.

Insurers are not allowed to apply more restrictive cost-sharing, waiting periods, or dollar limits to infertility care than those applied to other medical services.

Self-insured (ERISA) employer plans are exempt from this requirement but may choose to offer similar benefits voluntarily.

Companies that offer IVF Insurance

Many U.S. corporations offer comprehensive insurance coverage for in vitro fertilization (IVF) and other fertility treatments.

Ten companies known for their exceptional fertility benefits, include:

- Starbucks: Financial support for IVF, surrogacy, and adoption, with benefits available to both full-time and part-time employees.

- Walmart: Fertility benefits, including IVF coverage.

- Google: Comprehensive fertility benefits, including coverage for IVF treatments, egg freezing, and surrogacy assistance.

- Microsoft: Extensive fertility benefits, covering IVF treatments and related services.

- Facebook (Meta): Generous fertility benefits, including coverage for IVF, egg freezing, and adoption assistance.

- Apple: Comprehensive fertility benefits, covering IVF treatments, egg freezing, and surrogacy assistance.

- Amazon: Fertility benefits, including coverage for IVF treatments and related services.

- Johnson & Johnson: Fertility benefits, including coverage for IVF treatments.

- Salesforce: Comprehensive fertility benefits, including coverage for IVF treatments and related services.

- Bank of America: FullfFertility benefits, including coverage for IVF treatments.

What to Do If Insurance Doesn’t Cover IVF?

For patients whose insurance does not cover IVF, alternative options include:

Lower cost clinics: CNY Fertility offers IVF at 1/3 the national average. For many people the total out-of-pocket costs at CNY rival the insurance deductibles at more expensive clinics.

Payment plans and clinic financing: Many fertility clinics, including CNY Fertility, offer flexible financing or bundled packages to reduce costs.

Fertility grants: Nonprofit organizations and fertility-focused grants may help cover a portion of treatment expenses. There are numerous grants available to LGBTQ couples. The CNY Fertility IVF Grant is open to all applicants.

Does Insurance Cover IVF? The Bottom Line

Navigating insurance coverage for IVF can be complex, but understanding your options is key to managing costs and accessing care. Coverage varies widely based on state mandates, employer-provided benefits, and the type of insurance plan you have. If your insurance does not cover IVF, alternative options such as lower-cost clinics, payment plans, and fertility grants can help make treatment more affordable and accessible, bringing you one step closer to building the family you envision.